Check Your Homeowner’s Insurance Policy Before the Next Storm Hits: Does Your Roof Have Full Replacement Coverage?

- Staff

- Feb 22

- 5 min read

Most homeowners assume that if their roof is destroyed by hail or wind, their insurance company will simply pay to replace it.

Unfortunately, that assumption is becoming increasingly dangerous.

Over the past several years, I’ve seen a growing number of policies that do not fully cover roof replacement, even when the roof is clearly totaled by storm damage. Many homeowners only discover this after filing a claim — when they’re suddenly facing thousands (or even tens of thousands) of dollars in unexpected out-of-pocket costs.

After 21+ years as an exterior insurance restoration contractor, I can tell you this trend is real — and it’s accelerating.

If you own a home, now is the time to review your homeowner’s insurance policy.

The Shift Away From Full Replacement Value (RVC) Roof Coverage

Traditionally, most homeowner’s insurance policies provided Replacement Value Coverage (RVC) for roofs. That means:

If your roof is damaged beyond repair,

And the damage is covered under your policy,

The insurer pays the full cost to replace it (minus your deductible).

Today, however, many insurance carriers are quietly shifting to more restrictive roof coverage models.

These policies go by different names, but they all have the same result:

You could be responsible for a substantial portion of your roof replacement — even when the damage is fully covered.

Common Roof Coverage Limitations Homeowners Should Watch For

Here are the most common policy types I’m seeing:

1. Actual Cash Value (ACV) Roof Coverage

With ACV roof policies, the insurance company only pays the depreciated value of your roof — not the cost to replace it.

For example:

Roof replacement cost: $18,000

Roof age: 15 years

Depreciation applied: 50%

You may receive only $9,000 (minus your deductible).

That leaves you responsible for the rest.

This is one of the most common limitations we’re seeing today.

2. Roof-Specific Percentage Deductibles

Some policies now include a separate roof deductible, often a percentage of your home’s insured value.

Example:

Home insured for $400,000

2% roof deductible

Your out-of-pocket before coverage begins: $8,000

That’s before any other policy limitations apply.

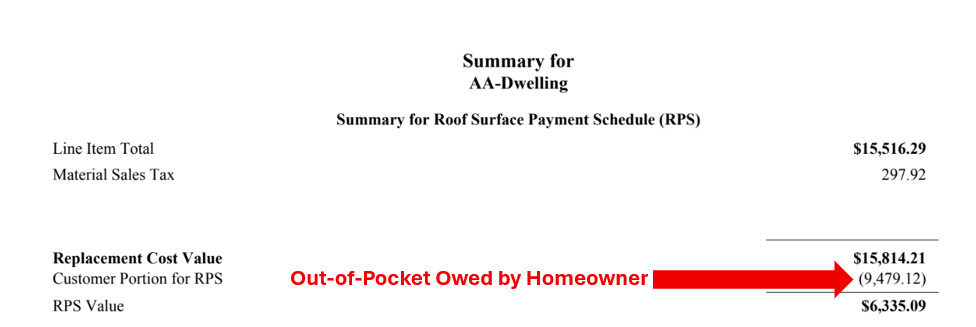

3. Roof Payment Schedules (Age-Based Payouts)

Certain insurers use roof payment schedules, which limit payouts based on roof age.

For example:

0–5 years old: 100% replacement

6–10 years old: 80%

11–15 years old: 60%

16+ years old: 40% or less

Even if your roof is completely destroyed by hail, the payout may be capped.

4. Minimum Out-of-Pocket Requirements for Roof Claims

Some policies include provisions where the homeowner must absorb a pre-determined minimum amount specifically for roof claims — separate from or in addition to the standard deductible.

These may be described differently in the policy language, but the outcome is similar: the homeowner shoulders a much larger financial burden than expected.

Insurance Companies Where These Policies Are Commonly Seen

Policy structures vary by state and individual underwriting guidelines. However, based on field experience, these types of roof limitations are frequently seen with:

Allstate (800) 255-7828

American Family Insurance (800) 692-6326

Farmers Insurance (888) 327-6335

The Hartford (800) 243-5860

Liberty Mutual (800) 290-7933

Nationwide (877) 669-6877

Safeco (800) 332-3226

State Farm (800) 782-8332

Travelers (800) 842-5075

USAA (800) 531-8722

Not every policy from these carriers includes roof limitations — but many do. The only way to know is to review your specific policy.

Why This Matters More Than Ever

Storm activity continues to increase across many regions. When hail or wind damage hits, you don’t want to discover that your “full coverage” policy isn’t actually full roof coverage.

Many homeowners have no idea their roof coverage changed at renewal.

In some cases, policyholders were never clearly told they were moved to ACV or limited roof payout structures.

If your insurer reduced your roof coverage without clearly explaining it, you may want to reconsider whether that company is the right long-term partner for protecting your home.

Questions to Ask Your Insurance Agent Today

Call your agent and ask these specific questions:

Do I have Replacement Cost Value (RCV) coverage on my roof?

Is my roof covered at Actual Cash Value (ACV)?

Is there a separate roof deductible?

Is there a roof payment schedule based on age?

If my roof is completely damaged in a hail storm, will it be fully replaced minus my deductible?

If the answer is anything other than “Yes, you have full RCV coverage,” ask what it would cost to upgrade.

Why it pays to hire an exterior insurance restoration contractor for your hail or wind damage claim.

In many cases, paying slightly higher premiums for full RCV roof coverage is well worth it.

Don’t Wait Until After the Storm

Insurance policies are contracts. Once damage happens, you’re bound by the terms already in place.

Review your coverage now — before you need it.

If You’ve Recently Experienced Storm Damage

If your home has recently sustained hail or wind damage to your roof or siding, it’s important to:

Document visible damage

Prevent further interior water intrusion

Understand what your policy covers before proceeding

If you’re unsure about the condition of your roof or siding, a professional inspection can help you understand your options. If you live within our service area, call us at (877) 846-9566 or schedule a free inspection or estimate online.

We currently service these MD and PA counties:

Maryland Counties

Anne Arundel County, MD

Baltimore County, MD

Carroll County, MD

Cecil County, MD

Frederick County, MD

Harford County, MD

Howard County, MD

Montgomery County, MD

Pennsylvania Counties

Chester County, PA

Lancaster County, PA

York County, PA

Final Thought

Your roof is one of the most expensive components of your home.

Make sure your insurance policy treats it that way.

Paying a little more now for full Replacement Value Coverage could save you thousands later — and potentially spare you from a devastating out-of-pocket expense when you least expect it.

Disclaimer

Neither JP Construction nor its employers or employees are insurance producers, licensed agents, or adjusters. The information above is based on professional opinions founded on 21+ years in business as an exterior insurance restoration contractor working directly with homeowners and insurance carriers on storm-related claims.

Every policy is different. Always consult your licensed insurance professional for advice specific to your situation.